How surging demand from EVs and data centres is reshaping Europe's electricity grid

Grid Edge Europe takes a new perspective on sources of energy demand

1 minute read

Oliver McHugh

Senior EV Charging Research Analyst

Oliver McHugh

Senior EV Charging Research Analyst

Oliver analyses the global EV charging market, with a focus on North America.

Latest articles by Oliver

-

Opinion

European Power & Renewables: what to look for in 2026

-

Opinion

How surging demand from EVs and data centres is reshaping Europe's electricity grid

-

Opinion

Power from the people: the state of the vehicle-to-everything (V2X) market

-

Featured

Grid edge 2025 outlook

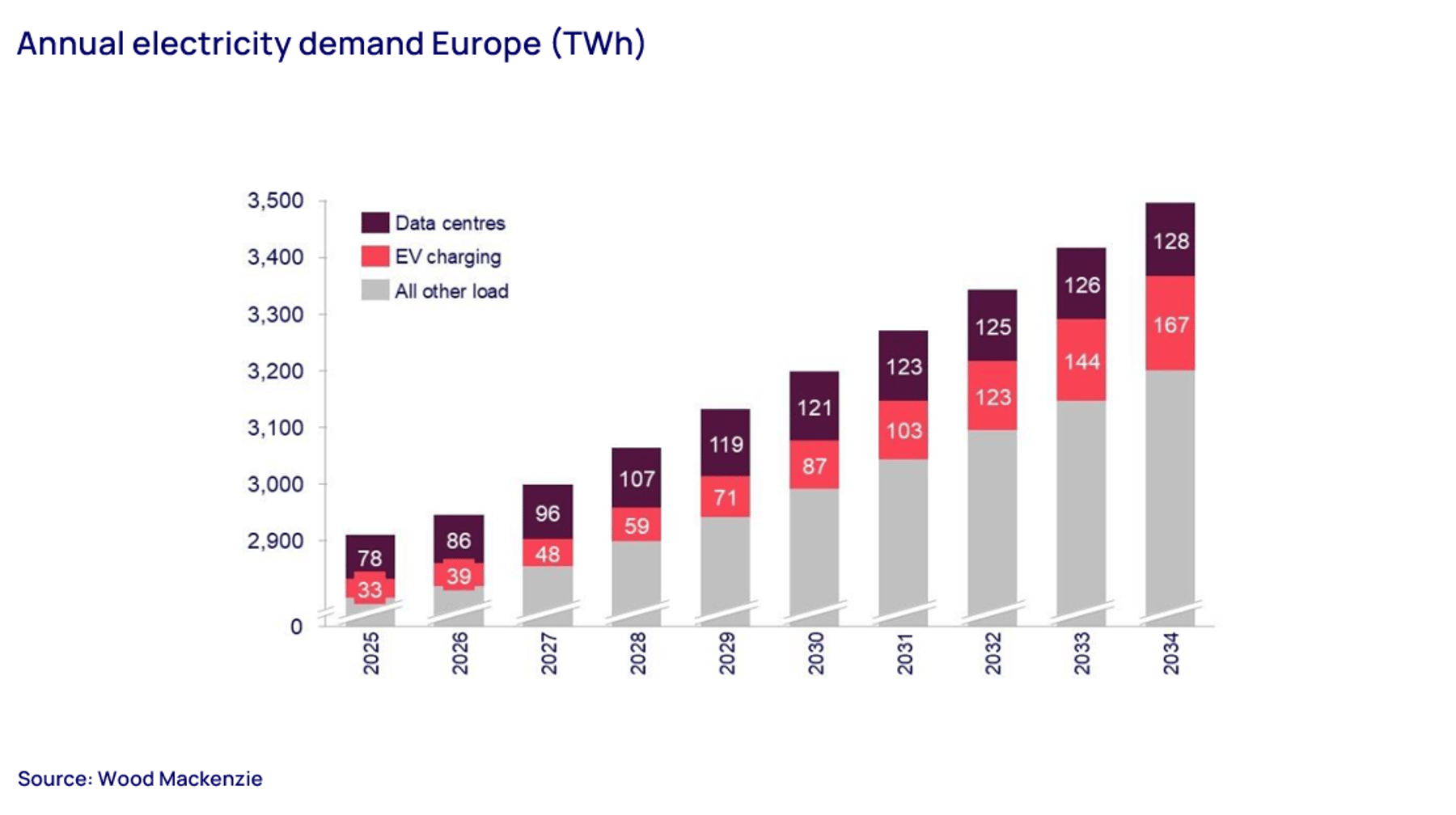

Electrical vehicle (EV) charging and data centres have emerged as key new loads on Europe’s electricity grid, meaning demand flexibility will be crucial to ensuring future grid stability.

In a new perspective on the electricity grid, Wood Mackenzie’s Grid Edge Europe team has taken an in-depth view on this new demand and what will be required to meet it. Fill in the form to receive a selection of complimentary slides from our inaugural report.

{kind=link}

Electrifying European transport

Installations of direct-current (DC) chargers are set to slow somewhat in 2025 after two years of rapid growth, as charge-point operators (CPOs) focus on profitability over network expansion.

The year 2024 saw some of the lowest ratios of battery electric vehicles (BEVs) to direct-current fast chargers (DCFCs) across the continent, though an increase in BEV sales in 2025 should start to reverse this trend. Ratios vary greatly from country to country.

The Netherlands and Belgium have a low number of DC chargers compared with the size of their BEV fleets. Arguably, their prioritisation of alternating-current (AC) charging infrastructure means DC chargers are less important to their overall charging strategy.

After a slower start, the UK has picked up the pace. Grid connection issues and ambiguous subsidy support have hampered progress, however. The government’s ‘Project Rapid’, announced in 2023, promised to support large grid connections for CPOs, but ran into issues and was eventually shelved.

Germany and France have the largest public DC charging networks in Europe. Both saw strong installation growth in 2023 and 2024, but are set to see a slight slowdown in 2025. Even so, the outlook for the DC market there is good, amid strong policy and industry support.

The EV market in Italy has been sluggish. There was strong growth in DC installations in 2024, but the removal of the ‘bonus colonnine’ subsidy in November 2024 means 2025 installations are likely to slip.

Nonetheless, Europe's public EV charging infrastructure should see a compound annual growth rate of 10.7% between 2025 and 2040. We estimate that EV charging will account for 9% of all electricity demand in the top nine European EV markets by 2040.

The data centre draw

The European pipeline for data centre projects across five countries (the UK, Germany, Spain, France and Ireland) amounts to 26 GW, although many of these are unlikely to be realised. Around 7 GW of this capacity has been announced (across these five markets) since just the end of 2024.

Monthly additions in proposed capacity are growing by 41 MW per month, driven by more projects being disclosed (+0.2 projects/month) and those projects being larger on average (+2.6 MW per project per month). Risk-adjusted forecasts suggest that demand will almost double in the next five years to 75 TWh.

Data centres dedicated to AI have a greater need for power than other use cases. They account for 10% of proposed sites but 25% of proposed capacity, and are set to have a disproportionately large impact on electricity demand relative to the number of pipeline projects.

More than 50% of sites in development since 2023 operate under colocation models (where operators rent standardised space units to multiple tenants). The number of disclosed AI-dedicated sites has quadrupled from a low base since the beginning of 2024, outpacing growth in all other segments, while cloud activity continues a slower, steady climb.

Demand-side flexibility will be key

The opportunity for demand-side flexibility (DSF) varies significantly, but remains underutilised. We forecast 9% compound annual growth in the capacity of DSF to 2050.

France is a mature market for DSF, but revenue is expected to fall due to capacity market reform in 2026. France operates a decentralised capacity market (CM) in which electricity suppliers must procure sufficient capacity guarantees to meet peak demand. The CM is currently open and accessible to DSF and independent aggregation.

In Germany, high wholesale volatility presents an opportunity. Currently, DSF must participate in the wholesale market through their electricity supplier. Independent aggregation is not allowed. Low smart-meter penetration is a key barrier to participation. As of 2025, fewer than 20% of customers with consumption in excess of 6,000 kWh had a smart meter installed. However, 95% of such customers should have a smart meter by 2030.

The creation of the Virtual Trading Party (VTP), meanwhile, makes wholesale markets the key driver of DSF in the UK, allowing independent aggregators to access the wholesale market. This unlocks a larger value pool for demand-side assets. The VTP framework establishes a “mutualised compensation pot” and does not require the VTP to contract with an asset’s supplier before using it in the wholesale market.

Learn more

To learn more and to receive a complimentary selection of slides from our inaugural Grid Edge Europe report, fill in the form on this page.

Plus, discover our new Lens Data Center and Data Campus Maps feature, which lets you examine where large electricity demand loads may be placed on the power grid in North America, Europe and Asia to uncover investment opportunities and analyse impact.